- AMZN trades near $230, with improving profitability and strong cloud/AI momentum entering 2026.

- 2026 forecast targets $250 - $300, supported by 10-12% revenue growth and rising margins.

- Long-term models show AMZN could reach $430 - $500 by 2030, driven by AWS and AI expansion.

- By 2040, AMZN may climb above $1,000, based on historical compounding and cloud leadership.

Table of Contents

- Amazon Live Chart

- Amazon Stock Forecast 2026

- Amazon Stock Forecast 2030

- Amazon Stock Forecast 2040

- AWS & AI Revenue Growth

- Wall Street Analyst Ratings

- Frequently Asked Questions

- What is the Amazon stock prediction for 2026?

- Will Amazon stock reach $500 by 2030?

- Does Amazon stock pay dividends?

- Is Amazon a good long-term buy right now?

Amazon Live Chart

Amazon (AMZN) peaked at $254 on November 3, 2025 and is trading around $230 as of December 2025 (StockAnalysis.com). The stock has gone through a wild five-year cycle: a COVID-19 induced rocket in 2022 – 2021, followed by a brutal correction in 2022 and now what ought to be the start of a powerful multi year recovery from 2023. With profit outlook brightening and cloud and AI services both growing rapidly. Amazon is entering 2026 with good impetus for positive long-term outlook.

Amazon Stock Forecast 2026

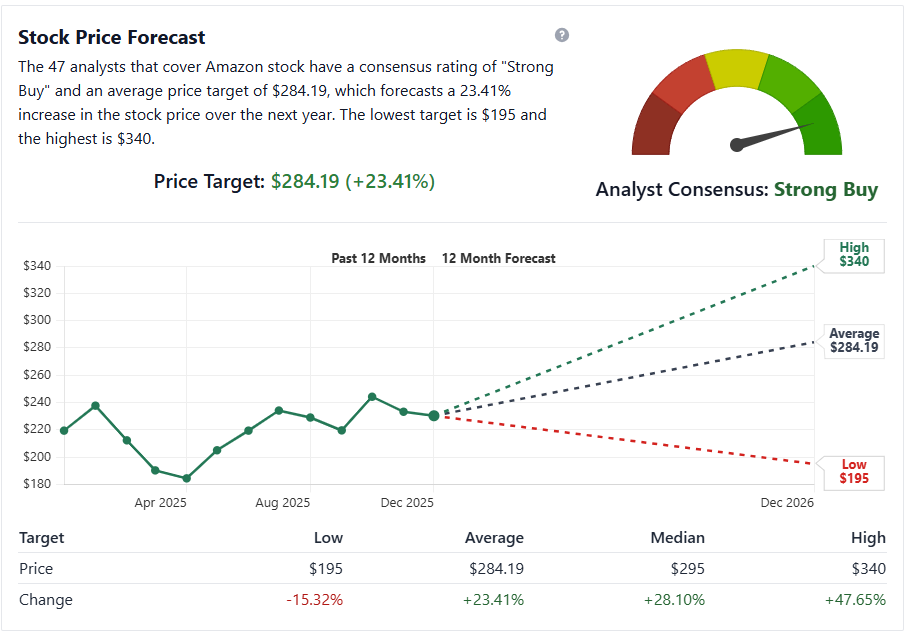

Amazon’s near-term picture is stable and has a slight bullish bias analyst project about 10 to 12% annual revenue increase as AWS increases and e-commerce starts becoming leaner (StockAnalysis.com). The 12-month consensus price target is about $280 to $285, implying around 20% upside from current levels.

Increasing profitability bolsters this prediction: Amazon’s most recent quarterly net margin surged to 11.1%, driven by cost of declines and AWS’s superior economics (Yahoo Finance). Absent any macroeconomic or regulatory earthquakes, Amazon is likely to grind higher through 2026 rather than making some staggering move. The typical valuation model would tag AMZN in the $250-$300 range in late 2026, where it belongs given its continued e-commerce dominance growing ad business and robust demand for cloud services.

Amazon Stock Forecast 2030

The core battlefield of Amazon’s future value is not whether it can achieve that $500 billion number by 2030. Most analysts think it is possible, unless the growth surprises on the downside. The popular scenario we read about speculates that if operating income (the accounting variety) were to reach something on the order of $200 billion before 2030, “Amazon’s market capitalization could vault up to $5 trillion by this decade’s end, valuing each share in the range of $430-$500” (UltimaMarkets.com). Other models like CoinCodex’s tech-sector growth predictions, suggest similar long-term numbers when plugging in annual returns over around 15%.

There is evidence from investment professionals to back this up. Independent equity researchers and LinkedIn aces suggested if Amazon maintains 10% revenue growth and grows op margins into the mid-teens, you would garner more than 100% by 2029 — and works out close to a $480-$500 price in early January of 2030.

Not all predictions are quite so robust. Even more tempered long-term views only anticipate Amazon at $300-$350 heads up, should cloud growth stall or valuation multiples shrink (UltimaMarkets.com). Even more conservative models (like the one from 24/7 Wall St.) model $250-$300 by 2030 prices if competitive pressures, margin compression were to put pressure on performance. Extremely bearish cases, which are few and far between among analysts, put AMZN at a point of less than $200 if certain business segments do not open as expected.

The wide ray of possibilities still leaves the prevailing opinion among institutional research that sustained AWS expansion and ongoing advertising growth provide a plausible path to $400-$500 per share by 2030.

Amazon Stock Forecast 2040

Predicting Amazon’s value 15 years from now is difficult, but useful for getting an idea of its long-term prospects. If Amazon were to grow at somewhere around the historical S&P 500 return of 11% per year, then we could reasonably expect Amazon to be worth about $1200 in the year 2040 (CoinCodex.com). This is based on the idea that Amazon continues to win in e-commerce, cloud computing and digital advertising, while creeping into new areas like healthcare and AI powered business services.

Under more generous assumptions — say, return to a tech sector’s long-run average annual growth rate of over 15% — Amazon’s valuation could skyrocket and theoretically push the stock past $2000. Those levels imply a future market cap of $10-$12 trillion, which is hard to fathom today, but not implausible over a 15 year-horizon, so long as Amazon can maintain its technology and platform leadership.

A less-optimistic view recognizes the substantial and uncertainty associated with decades-to-centuries projections. The growth rate may decline the single digits even by the 2030s, which would barely be sufficient to support AMZN and above current levels by 2040. Macroeconomic cycles, regulatory restrictions and increased competition in the cloud are unpredictable longer-term risk as well. A more balanced perspective sees Amazon well over $1000 by 2040 under reasonable growth assumptions, but notes that such long-term forecasts need to be frequently reviewed.

AWS & AI Revenue Growth

One of the crucial supports for Amazon‘s long-term valuation is the persistence of AWS’s dominance. AWS’s revenue re-accelerated in recent quarters to 30% Y/Y, driven in part by increasing enterprise AI workloads (Amazon IR). While AWS is less than 20% of companywide revenue for Amazon, it’s frequently 50% to 70% of overall operating profits due to AWS margins that are reliably higher than 25 to 30% (LinkedIn analyst research).

Cloud dominance also continues: 30% of the global cloud market share belongs to AWS, than the figures Microsoft Azure and Google cloud hold.(UltimaMarkets.com). This firm stands provides Amazon with a lasting edge as global AI infrastructure spending grows.

Amazon’s investments in AI provide even more upside. The latter was to invest $8 billion into Anthropic over the 2023 to 2024 period, effectively becoming AWS leading computer provider (Reuters). The alliance further solidified AWS’s lead in basic AI models and was estimated to drive a $9.5 billion valuation uplift for Amazon in 2025 (Amazon IR). Anthropic models and used on Amazon Bedrock with support for Amazon’s Trainium an Inferentia chips, extending Amazon’s AI ecosystem while expanding AWS’s high margin services.

The confluence of AI and cloud places Amazon not just as a retail and logistics monster but a global, ageless platform for the world’s embrace of artificial intelligence, which is also why analysts love Amazon so much farther out.

Wall Street Analyst Ratings

Wall Street remains generally bullish on Amazon. Out of 47 analysts tracked, 46 said buy or strong buy while none recommended sell (StockAnalysis.com). The average 12-month price target is $284 and even with high-profile upgrades such as those from MorningStar and well-known banks that maintain Amazon separately at buy rated, well naming it a top conviction idea due to improving margin retail, accelerating AWS growth, not to mention its unmatched scale within high value tech segments.

In general, Amazon is still seen as a long-term core holding with great compounding potential — one of the few mega-caps that continues to provide growth and some safety.

Frequently Asked Questions

What is the Amazon stock prediction for 2026?

Analysts aspect Amazon to trade around $250-$300 supported by 10 to 12% annual revenue growth and expanding margins.

Will Amazon stock reach $500 by 2030?

Yes — many long-term models show AMZN reaching $430-$500 by 2030, primarily driven by AWS and AI expansion.

Does Amazon stock pay dividends?

No. Amazon maintains a strict-no-dividend policy, re-investing profits into growth areas such as AWS, logistics and AI.

Is Amazon a good long-term buy right now?

Most analyst say yes with AWS profitability, strong AI positioning and unanimous buy ratings. Amazon remains a compelling long-term investment for patient shareholders.

AAPL

AAPL MSFT

MSFT META

META ^NDX

^NDX BTC-USD

BTC-USD XRP-USD

XRP-USD SUZLON.NS

SUZLON.NS INR=X

INR=X EURUSD=X

EURUSD=X JPY=X

JPY=X CAD=X

CAD=X